Government Bonds Are Back

Four converging forces are quietly ending the worst bond bear market in 150 years

I woke up Saturday morning to my phone buzzing with news alerts. A war had broken out overnight in the Middle East, the kind that changes things. Equity and bond markets were closed. The only thing trading was crypto, and watching Bitcoin tick up and down in real time while the world’s most consequential asset markets sat frozen felt surreal. There was nothing to do but think.

The obvious plays were already clear to everyone. Oil. Defense. Gold. Crypto catching a bid on dollar uncertainty. Every financial feed was running the same playbook. But one asset class, historically the most classical safe haven of all, was barely mentioned. Nobody was talking about bonds.

I have been studying government bonds intensively for months, building a thesis piece by piece. And Saturday morning was the moment I asked myself: is this the piece missing from most portfolios right now?

Government bonds. Long duration ones.

I know. Bear with me.

The Asset Class Everyone Buried

Cast your mind back to 2022. The Federal Reserve, having spent most of 2021 insisting inflation was “transitory,” abruptly pivoted and delivered the most aggressive hiking cycle in four decades. Inflation hit 9.1% in the United States. The war in Ukraine sent energy prices spiraling. Supply chains were still fractured. The dominant macro variable, for the first time in decades, was inflation, and inflation is the enemy of both stocks and bonds simultaneously.

That dynamic is what made 2022 so uniquely brutal. For decades, bonds had served as portfolio ballast: when stocks fell, bonds rallied. That negative correlation was the entire foundation of the 60/40 portfolio. In 2022, both legs buckled at once. Long-duration US Treasuries fell over 29%. The 60/40 portfolio suffered its worst drawdown in 150 years. To put that in perspective: it underperformed even an all-equity portfolio, something that had never happened in the entire recorded history of that strategy.

The verdict was swift and nearly unanimous. “Bonds are dead.” “60/40 is finished.” Serious investors. Serious institutions. And for a moment, they were not wrong.

But the conditions that killed bonds were specific: a once-in-a-generation inflation shock combined with the most aggressive tightening cycle in forty years. Those conditions are now structurally reversing. Four forces are converging that I believe mark the beginning of a structural bull market in long-duration sovereign debt.

Force 1: Geopolitical Shock, Flight to Safety, and Why Oil Does Not Break the Thesis

A major war has broken out in the Middle East. The trajectory is genuinely unclear. A protracted conflict, potential energy supply disruptions, and regional spillovers create an immediate, sustained bid for safe haven assets. In a world of rising uncertainty, capital does not reach for yield. It reaches for certainty. And the most liquid, most trusted certainty in global finance remains a government bond from a stable sovereign.

The natural objection is oil. A conflict threatening the Strait of Hormuz sends energy prices higher, and energy price spikes are inflationary, the exact regime that punished bonds in 2022. Brent crude is already up roughly 19% year to date even before this weekend. Is this not a bond headwind, not a tailwind?

Here is why I think this objection, while real, does not break the thesis.

Long-duration bonds do not price next quarter’s CPI. They price what the market believes inflation will average over the next 15 to 30 years. An oil spike, even a severe one, is a short-term supply shock. It shows up in headline inflation for months, perhaps a year or two. But a 30-year bond is not pricing whether Brent hits $120 in 2026. It is pricing the structural inflation trend over a generation.

On that timeframe, a short-term energy spike is a complication to monitor, not a reason to abandon the thesis. If anything, near-term volatility may simply create a better entry point.

The first tailwind is blowing.

Force 2: The Citrini Scenario: A Tail Risk Worth Pricing

Last week, a Substack post went viral enough to actually move markets. Citrini Research published a fictional dispatch from June 2028 looking back at an AI-driven economic catastrophe: mass white-collar displacement, a hollowed-out consumer base, a deflationary spiral, the S&P 500 down 38%. Citrini called it the “human intelligence displacement spiral.”

Citadel Securities fired back with actual labor data. Software engineering job postings are up 11% year on year. AI daily use in workplaces is “unexpectedly stable.” The idea that this resolves catastrophically within 24 months strains credibility, and they are largely right.

I do not need to believe the Citrini 2028 scenario to find it useful. What matters is that this narrative is now in the market’s bloodstream. Even as a tail risk, it creates a structural bid for deflationary hedges. Long-duration government bonds are, by design, the most direct hedge against a deflationary demand shock. A tail risk that moves markets when articulated is a tail risk worth holding insurance against.

Force 3: Productivity-Led Deflation: The Base Case Nobody Is Discussing

The Citrini scenario is demand-destructive deflation. But there is another version of AI-driven deflation that is actually constructive, and it is arguably already happening. AI makes workers radically more productive, firms produce more output with fewer inputs, costs compress. This is the deflationary force that lifted living standards across the industrial and computer revolutions, and it is now beginning to emerge in the data.

Erik Brynjolfsson at Stanford recently argued that US productivity grew roughly 2.7% in 2025, nearly double the prior decade’s average, a decoupling of real GDP from labor input that is the classic signature of a productivity harvest phase. Goldman Sachs projects 0.3 to 3.0 additional percentage points of annual productivity growth from AI adoption.

The honest caveat: most macro studies still find limited aggregate evidence. Adoption remains shallow for most firms. The productivity J-curve may have years to run before it shows up clearly in price data.

But the direction of this force is unambiguously deflationary. A world where AI relentlessly compresses the cost of cognitive labor is a world where the structural inflation rate is lower over the long run than the 2022 shock suggested. And here is why this matters for instrument choice specifically: a 30-year bond prices what the market believes inflation will average over three decades, not next quarter’s CPI. If AI structurally lowers long-run inflation expectations, the 30-year bond is the instrument most directly and powerfully exposed to that repricing. You are not buying a rate cut. You are buying a civilizational bet on where prices go over a generation.

Force 4: Private Credit Cracks

Private credit has been one of the great post-2008 financial success stories, a $3 trillion market offering higher yields in exchange for illiquidity. For a decade, it worked brilliantly.

Now the cracks are showing. Blue Owl has moved to restrict redemptions. Software companies, roughly 25% of private credit portfolios according to S&P, are under existential pressure as AI undermines the moats that made them creditworthy. Many loans remain marked near par despite deteriorating fundamentals. Jamie Dimon has been warning about “cockroaches” in private credit for months.

When private credit stress builds into a genuine repricing, capital does not evaporate. It rotates toward the most liquid, most transparent, most sovereign end of the credit spectrum. The beneficiary is, almost mechanically, government bonds.

TLT, Bunds, or Both?

The two most accessible expressions of this thesis are TLT for US-based investors and core EUR government bonds for European or globally-minded allocators. Both were savaged by the same 2022 bear market. Both are near multi-year lows. Both benefit from the deflationary forces above.

TLT is the natural starting point for most readers. It is the most liquid long-duration vehicle in the world, with over $45 billion in assets, tracking US Treasuries with maturities of 20 years and above, currently yielding around 4.4%.

The honest counterargument for US bonds: America’s fiscal situation. Deficits are structural and large. The term premium has been rising. Treasury supply is enormous. For long-duration Treasuries, you are holding a tug-of-war between deflationary forces pulling yields down and fiscal dynamics pushing them up. The thesis still holds, but the headwind is real.

Core EUR government bonds, specifically German Bunds, French OATs and Dutch DSLs, offer a cleaner expression of the same thesis. The Eurozone’s institutional architecture, including the Stability and Growth Pact and the ECB’s mandate, creates a meaningfully lower probability of fiscal dominance. The ECB is further along its rate-cutting cycle. The same four deflationary forces apply, without the Treasury supply overhang.

TLT for simplicity and liquidity. Core EUR government bond funds for those who want the thesis without the fiscal tug-of-war. For US investors comfortable with the fiscal headwind, TLT is a perfectly valid expression of the same thesis. The EUR version is simply the cleaner trade.

Why Long Duration Specifically?

Think of duration as a sensitivity dial. A short-duration bond, say a 2-year Treasury or Bund, barely moves when rates change. It is close to cash: safe, but offering almost no price appreciation even if the deflationary thesis plays out perfectly. A long-duration bond in the 15-30 year range amplifies every basis point of rate decline into meaningful price appreciation. The same deflationary impulse that moves a 2-year bond by 1-2% moves a 30-year bond by 15-20%.

There is also convexity. Long bonds do not move linearly with rates. As yields fall, price appreciation accelerates rather than adding up mechanically. Your upside is larger than a linear calculation suggests, while your downside is bounded by the coupon you collect while waiting. TLT currently yields around 4.4%. IBCL.DE offers a weighted average yield to maturity of around 3.7% in EUR terms, lower than TLT but still a meaningful real coupon after years of near-zero rates on European debt. In 2020 and 2021, you held duration for near-zero yield and prayed for capital appreciation. Today, you are paid to be patient.

Short duration is safety. Medium duration is a hedge. Long duration is the conviction trade. If you believe the four forces described above are real, long duration is where the thesis pays.

What Would Make Me Wrong

Sustained oil shock: Strait of Hormuz disruption sends energy prices structurally higher, keeping inflation sticky at levels that prevent the Fed and ECB from cutting. Near-term noise becomes a long-run signal.

Term premium keeps rising: Even as growth slows, bond supply overwhelms demand, pushing long yields higher despite deflationary fundamentals. Fiscal dominance wins the tug-of-war, especially in US Treasuries.

AI deflation delayed: The productivity J-curve takes a decade, not two to three years. Long-run inflation expectations stay anchored rather than repricing lower.

Eurozone fiscal fracture: Peripheral spread widening destabilizes the EUR government bond complex, dragging core bonds into the repricing despite their stronger fundamentals.

Geopolitical resolution: A rapid ceasefire stabilizes oil markets and removes the safety bid faster than the structural thesis can take over. This would not break the structural case, but would remove the near-term catalyst.

I hold these risks seriously. But my probability-weighted view is that the convergence of the four forces above creates a regime shift that favors long-duration sovereign debt more than at any point in the last four years.

Where I Stand

Full transparency. For most readers here, the natural instrument is TLT. It is the most widely followed long-duration vehicle in US markets, deeply liquid, and a direct expression of the thesis.

iShares 20+ Year Treasury Bond ETF (TLT): down 36.54% over five years, still well below its 2021 highs near $150. YTD total return has turned positive at +4.60%, a tentative early signal. I do not personally hold TLT, but reference it as the primary instrument for US-based readers.

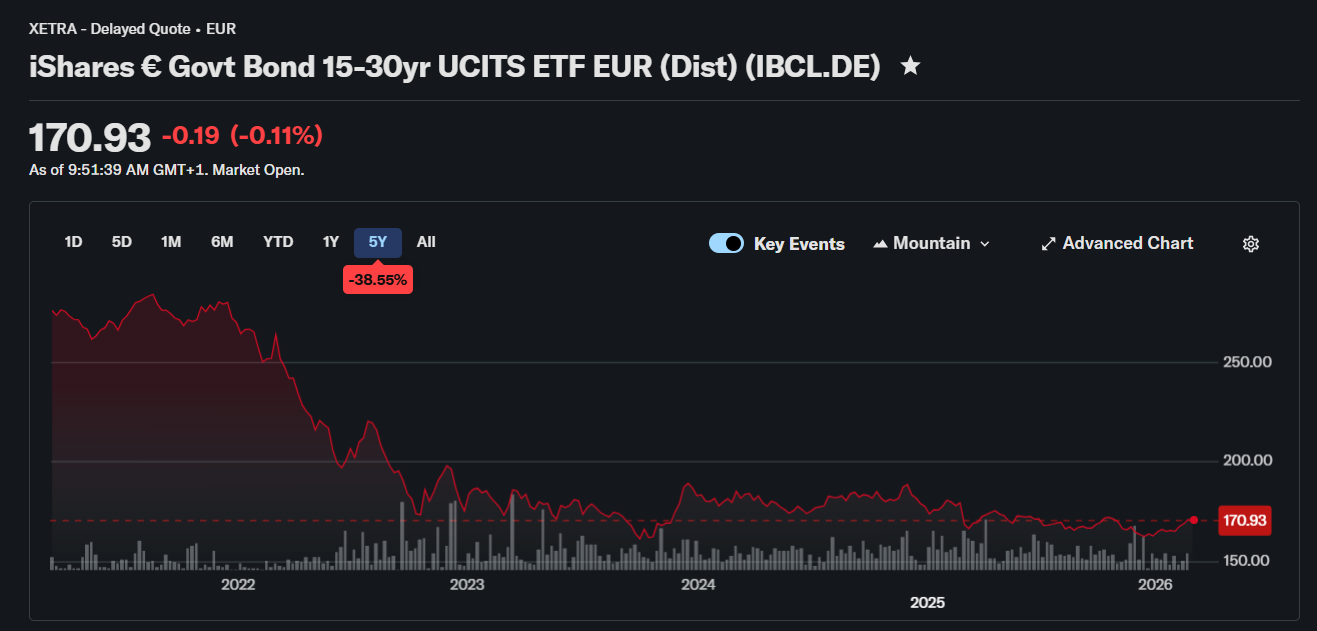

I am a Europe-based investor. My personal position is the iShares Euro Government Bond 15-30yr UCITS ETF, trading as IBCL.DE on Xetra or IBGL on the London Stock Exchange, which I hold as a meaningful weight in my portfolio.

iShares Euro Govt Bond 15-30yr UCITS ETF (IBCL.DE): down 38.53% over five years. The scar from 2022 is visible. So is the entry point.

Both charts say the same thing: a once-in-a-generation drawdown, with instruments still grinding near multi-year lows. The thesis does not require a precise bottom call. It requires a view on direction over the next two to three years.

I also hold gold and select commodity equities alongside. These are not competing with bonds for the same role. Bonds hedge deflation deterministically. Gold hedges debasement and sentiment-driven tail risk. Commodities hedge the inflationary geopolitical scenario I named in the bear case. No monocultures. Complementary positions for different failure modes of the current system.

The boring trade. The one nobody is discussing at the dinner party. The one that felt dead two years ago and is quietly, unmistakably, coming back to life.

I have been wrong before. But right now, four different forces are all pointing the same direction.

🙏 If this kind of analysis is useful to you, subscribing ensures you don't miss the next piece. Likes help others find it.

About Scarcity Thinker

Most investors chase what is obvious. Scarcity Thinker looks for what is structurally constrained, mispriced, or overlooked. Metals, equities, crypto, and fixed income when the thesis is there. No asset class religion. No hype. New pieces every Tuesday and Friday.

This is not financial advice. These are my personal views and positions. Do your own research. The world is genuinely uncertain right now, which, if you have read this far, is precisely the point.

Great breakdown! The inclusion of the primary instruments and the what would make me wrong section really add credibility to the thesis. Thanks for sharing this.

can’t wait to read it later! 🍻