The Last Bottleneck

Medicine has been billing for consequences. The cause is finally investable.

TL;DR

Aging is not inevitable wear. It is increasingly understood as a programmable information error at the cellular level, making longevity the most consequential investment thesis of this decade

The money is not in betting on which therapy wins. It is in owning the bottlenecks every therapy must pass through: manufacturing, AI-driven discovery, and regulatory execution

Core positions (70 to 75%): Thermo Fisher, Vertex, Eli Lilly, or IBB/BTEC as packaged exposure. Structural infrastructure that performs regardless of which scientific approach prevails

Speculative sleeve (25 to 30%): Oxford Biomedica, Recursion Pharmaceuticals, XBI, and VITA/Bio Protocol. Asymmetric bets on specific chokepoints

The most underappreciated risk is not scientific failure but regulatory capture extending commercialization timelines by a decade

I have spent years thinking about where value hides before the market finds it. Scarce infrastructure, constrained bottlenecks, the unglamorous companies that everything else depends on. But occasionally something stops me completely, not because it is subtle, but because it is so obvious that the market’s indifference to it becomes the puzzle.

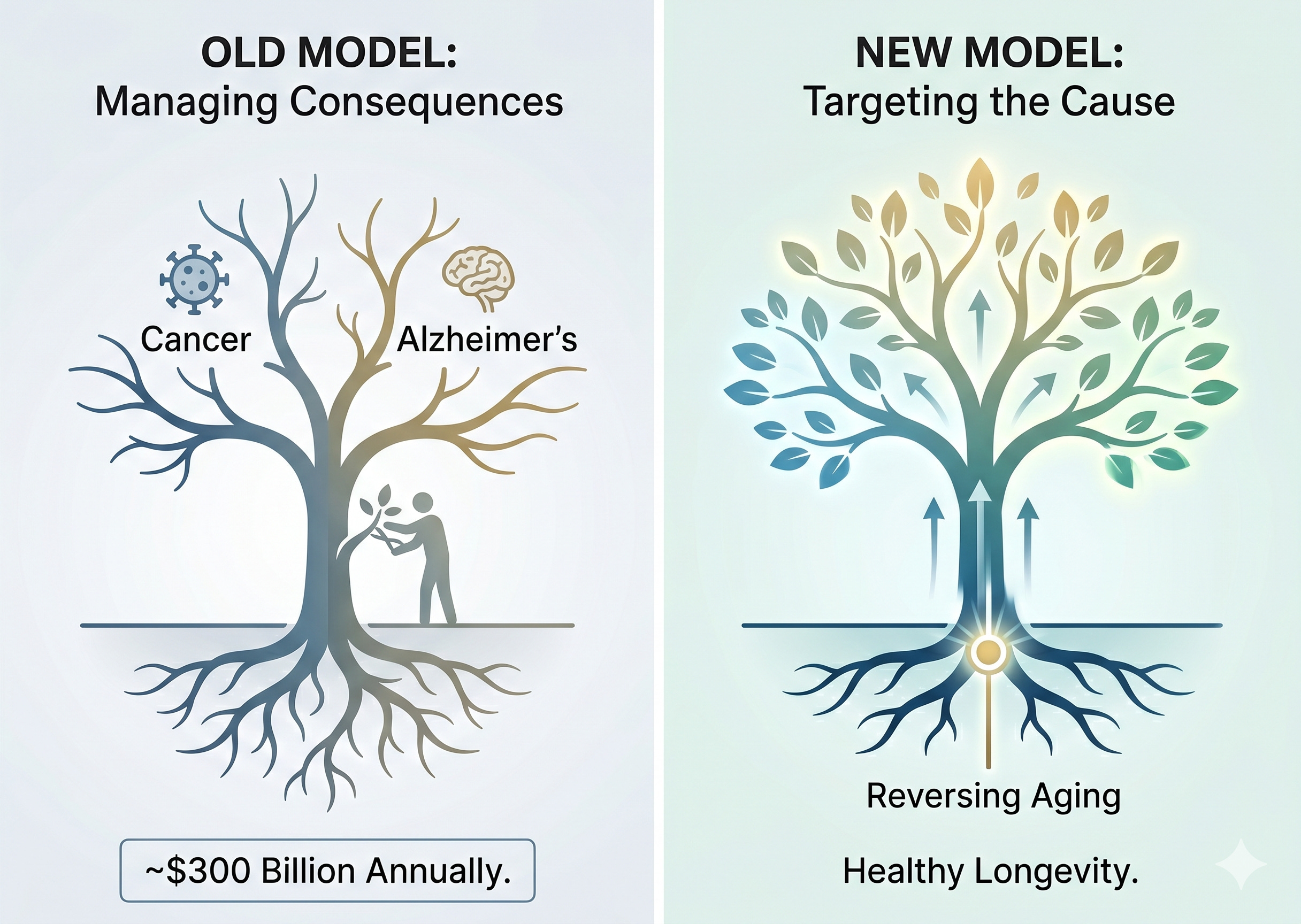

Try this calculation. Global cancer treatment is a market approaching $300 billion annually, built almost entirely on managing the disease rather than ending it. The companies doing the managing, the oncology drugs, the infusion centers, the follow-up diagnostics, are collectively worth trillions. Now ask what the company that actually cures cancer would be worth. Not manages it. Ends it.

There is no comparable number in financial history. And yet the infrastructure being built right now toward exactly that outcome, the manufacturing platforms, the AI discovery engines, the regulatory execution machines, is trading at completely ordinary multiples.

That gap is what this article is about.

Medicine has spent decades fighting fires while ignoring the arsonist. The diseases we name and treat are downstream consequences of a single upstream process. We have been billing for the consequences while the cause runs free.

That cause is aging itself.

We now understand, with increasing scientific confidence, that cardiovascular disease, Alzheimer’s, most cancers, and the cascade of conditions we associate with old age are not independent enemies to be fought one at a time. They are downstream consequences of a single upstream process: the gradual loss of cellular identity. The epigenome, the system that tells each cell which genes to activate, accumulates errors over time. Cells forget their jobs. The body begins manufacturing the diseases we have spent trillions trying to cure.

The biology has moved. The scientific consensus, slow as it always is, is catching up. And when a consensus shifts at this scale, from “aging is inevitable wear” to “aging is a programmable information error,” capital eventually follows.

The question is not whether to allocate to longevity. The question is how to do it without being burned by hype.

The Pickaxe Principle

History is consistent on this point. The defining fortunes of every transformative technology wave were not made by the companies that cracked the science. They were made by those who owned the infrastructure through which the science had no choice but to flow. The gold rush enriched the merchants selling shovels. The internet compounded for those who owned the cables, the chips, and the server farms. The genomics revolution of the 2000s minted money for sequencing equipment manufacturers long before any therapeutic reached market.

Longevity is entering exactly this phase. The core science of epigenetic reprogramming is real, but the path from laboratory result to scalable therapy runs through a series of hard physical, institutional, and computational constraints. Those constraints are the investment.

The most heavily funded private companies in the space confirm this indirectly. Altos Labs launched with $3 billion in starting capital backed by Jeff Bezos. Retro Biosciences, backed by OpenAI’s Sam Altman, is reportedly raising $1 billion at a $5 billion valuation. NewLimit raised $130 million in its Series B with Eli Lilly among the participants. None of these are publicly accessible. But they all flow through the same bottlenecks.

You do not invest in the promise of age reversal. You invest in the chokepoints.

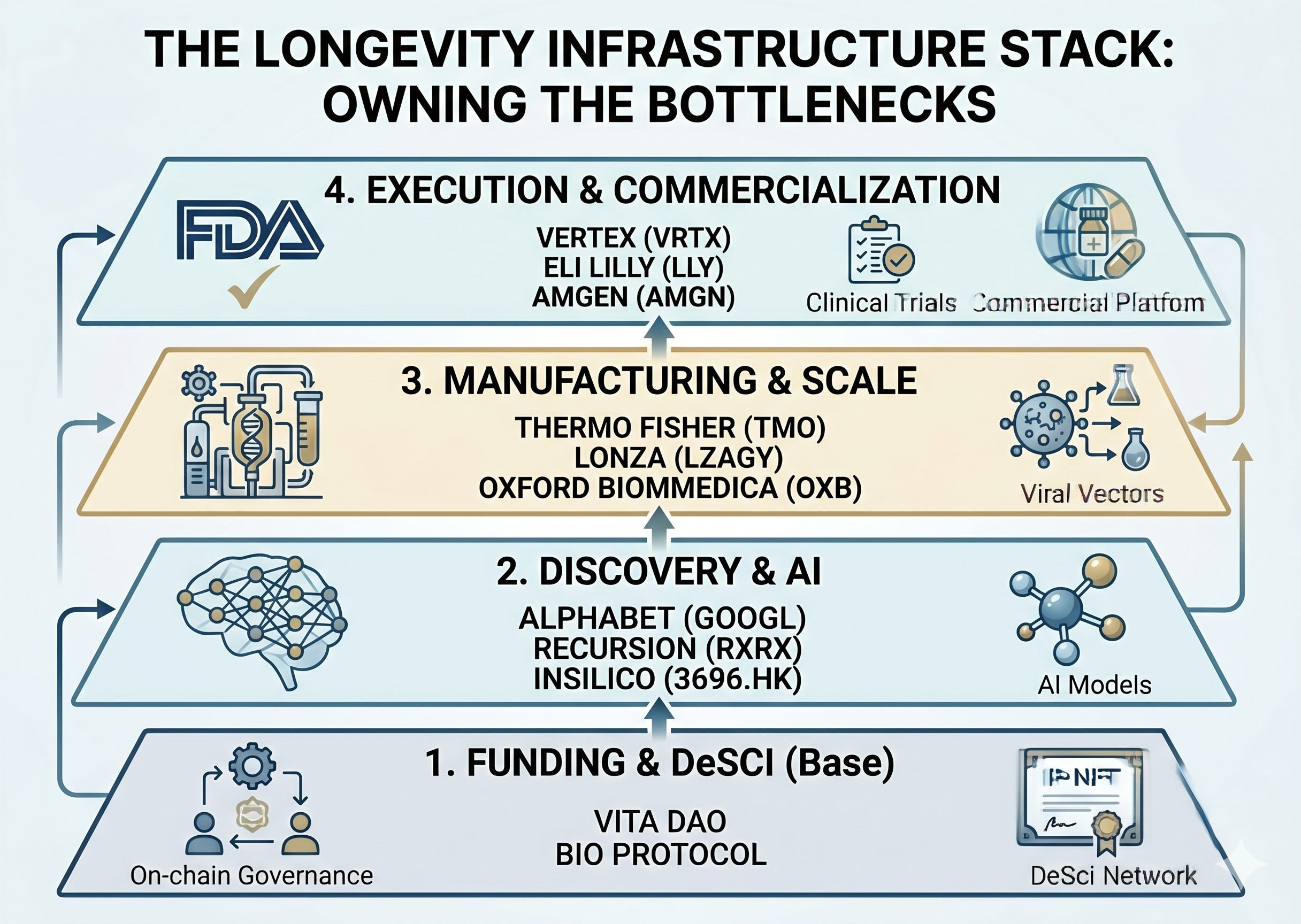

The pipeline runs in one direction: research gets funded or it dies, funded research identifies targets, targets get built into deliverable vehicles, vehicles get approved and reach patients. Each stage has a structural chokepoint. The sections that follow work through that pipeline from the most physically visible constraint backward to the most upstream one, from the factory floor where therapies are built, to the algorithms that find them, to the institutions that commercialize them, to the funding layer where the next generation of science either gets born or disappears quietly. Four bottlenecks. One stack.

Bottleneck One: Manufacturing (Making the Vehicle)

Before any longevity therapy can enter a human body, someone has to build the delivery system. For gene-based approaches, that means engineering adeno-associated virus (AAV) vectors, biological constructs that carry therapeutic genetic material into cells. These are among the most technically demanding products ever manufactured. Producing them safely and at clinical scale can cost upward of $10 million per trial, not for the trial itself, but just for the delivery vehicles.

This is not a problem that economies of scale will quickly dissolve. The manufacturing complexity is structural. These are not chemicals mixed to a specification; they are biological systems that must perform consistently across millions of doses in a regulatory environment where a single contamination event ends a program. Thermo Fisher and Lonza do not discover drugs and they do not sell them to patients. They make the biological machinery that other companies’ therapies are built from. They are upstream of everything and agnostic to which scientific approach wins. That agnosticism is precisely what makes them compelling.

Thermo Fisher Scientific (TMO) is the anchor infrastructure play, the dominant platform provider for the entire life sciences industry, AAV manufacturing included. It trades around $496 at a P/E near 28, roughly 12 to 14% below its historical average. For a structural monopoly, that is a modestly discounted entry.

Lonza Group (LZAGY) is the Swiss peer with a forward P/E around 28, well below the 40-plus multiples it commanded at peak biotech funding, and fairly valued relative to the strategic position it holds in the manufacturing stack. What makes Lonza particularly compelling for this thesis is the diversity of modalities it serves, from gene therapy to cell therapy to biologics, meaning its position strengthens regardless of which therapeutic approach eventually dominates.

Oxford Biomedica (OXB) is the speculative edge of this layer. No earnings yet, but a 30% revenue jump and EBITDA positive for the first time. Small allocation territory, but with genuine fundamental momentum behind the speculation.

The manufacturing bottleneck is the most physically durable constraint in the stack. Very few organizations in the world can do this reliably at scale, and building that capability takes years. It does not care which scientific approach wins. It just needs to exist for any of them to reach a patient.

Bottleneck Two: Discovery (The AI Engine)

The commercial endgame for longevity is not a $100,000 gene therapy. It is a $100 pill. Getting there requires identifying chemical compounds capable of replicating what genetic reprogramming does, at pharmaceutical cost and scale. No human team can screen the relevant molecular search space. This has become an AI problem.

The real scarcity here is not compute. It is proprietary biological datasets and the wet-lab infrastructure to validate what AI predicts. A model is only as good as the data it learned from, and the most relevant biological data in the world, cellular imaging maps, protein structure databases, clinical trial records, took decades and billions of dollars to generate. That data is the moat.

Alphabet (GOOGL) at a P/E of 29.3 is not primarily a longevity bet, but AlphaFold and Isomorphic Labs represent a scientific contribution of historic proportions. You are paying for the search business and receiving the AI biology optionality at no additional cost.

Recursion Pharmaceuticals (RXRX) is a pure-play bet on this thesis, currently trading around $3.75 with a market cap of approximately $1.9 billion. The automated cellular imaging library they have built is exactly the kind of scarce, non-replicable dataset that defines a long-term structural position. Whether the current capital structure survives long enough to monetize it is the real risk. This is high-conviction or do-not-touch territory, with no comfortable middle ground.

Insilico Medicine (3696.HK) is the name most investors in this space have not yet priced correctly. Listed on the Hong Kong Stock Exchange on 30 December 2025 in what was the largest biotech IPO in Hong Kong that year, raising approximately $293 million, it already has its first fully AI-discovered drug candidate in Phase 2 clinical trials for idiopathic pulmonary fibrosis. That is not a pipeline promise. It is a proof of concept. Access requires a broker with HKEX connectivity, which most major brokerages now support, and for investors who want exposure to the AI discovery layer with actual clinical validation behind it, Insilico is worth the extra step.

Bottleneck Three: Commercialization (Crossing the Finish Line)

Manufacturing produces the vehicle. Discovery identifies the target. But neither of those things puts a therapy in a patient’s hands. That requires something different: the institutional machinery to run late-stage clinical trials, absorb years of regulatory back-and-forth, build a commercial distribution network, and survive the process financially intact. This is not a scientific constraint. It is an organizational and financial one, and it is just as real.

The companies that have built this machinery are a scarce resource. Most biotech firms never develop it. They discover something promising and then license it, sell themselves, or watch their programs die in the regulatory process because they cannot sustain the years of capital expenditure and institutional friction that commercialization requires. The companies that can actually cross this finish line independently are the ones worth owning.

Pure-play epigenetic reprogramming remains largely private. The accessible exposure runs through large biotech platforms that have already proven they can take a novel therapy from clinical trial to commercial product at scale.

Vertex Pharmaceuticals (VRTX) is the most compelling risk-adjusted position here. A P/E of 28.5, near-monopoly economics in cystic fibrosis, and the successful commercialization of Casgevy, the first approved CRISPR therapy, prove that Vertex can do what most gene therapy companies cannot: build a commercial machine on top of a regulatory process. Revenue guidance for 2026 is pushing past $13 billion.

Eli Lilly (LLY) at 41.5x earnings is elevated but structurally supported by the cash flows that GLP-1 dominance generates. More relevant for this thesis is TuneLab, their internal AI drug discovery platform, and their participation in NewLimit’s Series B, a direct signal that Lilly is positioning across the commercialization and discovery layers simultaneously.

Amgen (AMGN) at 24x is the stability anchor: a mature biologics franchise, a solid dividend, and broad exposure to advanced therapeutics without the valuation risk attached to the higher-growth names.

Bottleneck Four: Funding (The DeSci Layer)

The longevity research ecosystem has a coordination problem that no individual company has solved: the most important biological data in the world is fragmented across competing private institutions, locked behind proprietary walls, and largely invisible to the researchers who need it most. Early-stage longevity research is systematically underfunded because the timelines are too long and the IP pathways too uncertain for conventional venture capital to bear. That funding gap, the valley of death between academic discovery and viable clinical trial, is as real a bottleneck as manufacturing capacity or regulatory bandwidth. It just kills science more quietly.

Decentralized science, or DeSci, is attempting to solve this directly.

VitaDAO, launched in 2021 and backed by investors including Pfizer Ventures, uses on-chain governance and token-based incentive structures to fund longevity research at the earliest, riskiest stages. To date it has deployed over $4 million across more than 20 research projects and built a treasury holding approximately $55 million in assets, including tokenized intellectual property through a framework of IP-NFTs. The governance token VITA allows holders to vote on which research proposals receive funding and how the resulting intellectual property is licensed and commercialized. The Bio Protocol, in which VitaDAO is a leading participant, is building a broader open financial network for programmable biology, aiming to make the entire DeSci ecosystem more liquid and accessible.

The other three bottlenecks are being addressed by institutional capital: Thermo Fisher and Lonza on manufacturing, Recursion and Alphabet on discovery, Vertex and Lilly on execution. The funding bottleneck is where institutional capital structurally cannot go, because the timelines are too long and the outcomes too binary. That is the gap DeSci occupies, and it is not a peripheral concern. It is where the next generation of longevity science either gets born or dies quietly.

The investment expression right now is primarily VITA, with broader exposure through the Bio Protocol ecosystem. Sizing should reflect genuine uncertainty: this is early infrastructure for a coordination experiment that has not yet proven its model at scale. The analogy is not buying Amazon in 1997. It is buying domain names in 1994, possibly transformative, possibly irrelevant, and worth being honest about which one you are doing.

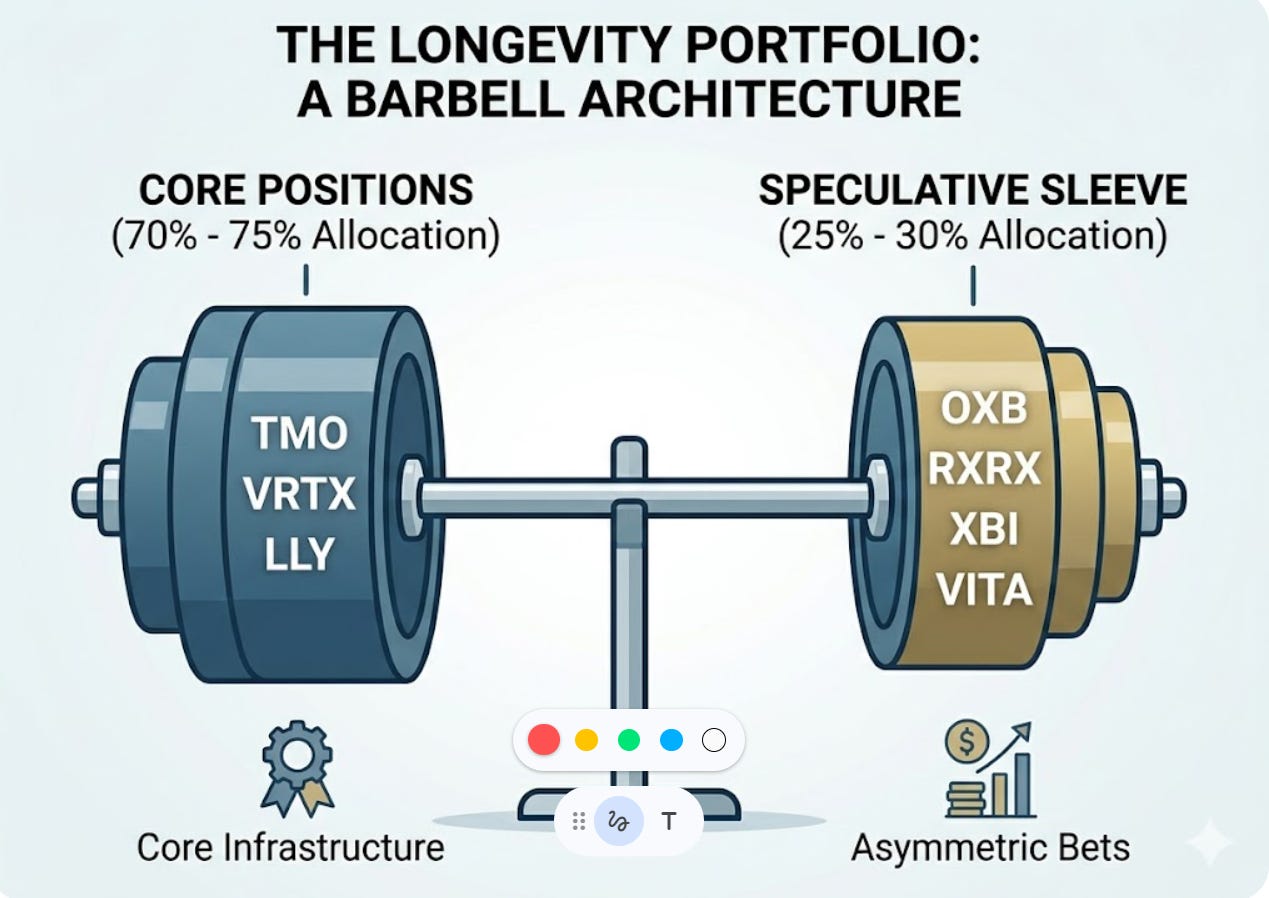

The Portfolio Architecture

The portfolio proposed across these four bottlenecks is a barbell, and that structure is the only rational one for a thesis this early.

The four bottlenecks are not separate investment ideas. They are a single stack, and the portfolio spans all of them deliberately. Manufacturing is covered by Thermo Fisher, Lonza, and Oxford Biomedica. Discovery is covered by Alphabet, Recursion, and Insilico. Execution is covered by Vertex, Lilly, and Amgen. Funding is covered by VITA and the Bio Protocol ecosystem. Each position has a specific structural rationale. None of them requires the same scientific outcome to perform.

For investors who prefer packaged exposure over individual stock selection, IBB is the natural vehicle for US investors: it tracks the Nasdaq Biotechnology Index across roughly 270 holdings, has over $5 billion in AUM, charges 0.45% in expenses, and its top positions, Amgen, Gilead Sciences, Vertex Pharmaceuticals, and Regeneron, map directly onto the execution and manufacturing bottlenecks. For European and non-US investors, the direct UCITS equivalent is the iShares Nasdaq US Biotechnology UCITS ETF (BTEC), listed on the London Stock Exchange, tracking the same index at 0.35% in expenses. Both serve the same function: a single liquid instrument that packages bottlenecks one through three without requiring individual stock selection.

Two ETFs worth naming for what they are not: iShares Ageing Population UCITS ETF (AGED), with roughly 47% in health care and 42% in financials including life insurance and retirement planning, is a silver economy bet, not a longevity science bet. Global X Aging Population ETF (AGNG) is closer, with nearly 84% in health care, but its AUM of around $62 million and inclusion of healthcare REITs make it an imperfect instrument. Both price in the demographic consequences of an aging population rather than the possibility of reversing aging itself. That is a different thesis.

The core of the barbell, roughly 70 to 75% of whatever allocation you are making to this space, sits in fairly valued, cash-generating infrastructure: Thermo Fisher, Vertex, Lilly, or IBB/BTEC as packaged exposure. These do not require a specific scientific outcome to perform. The bottleneck they own is structural.

The speculative sleeve, 25 to 30%, takes asymmetric positions where the upside is large if the thesis develops: Oxford Biomedica and Recursion on the manufacturing and discovery side, XBI for broader early-stage biotech exposure across smaller names that may advance through trials or attract acquisition, and VITA with the Bio Protocol ecosystem for the funding layer. These are not diversified positions. They are specific bets on specific bottlenecks, sized to reflect that.

The most underappreciated risk in this thesis is not scientific failure. The science is progressing on multiple fronts simultaneously. The real risk is regulatory capture: the institutional layer tightening around these therapies in ways that extend commercialization timelines by a decade and price the eventual treatments beyond the reach of ordinary people.

That risk does not invalidate the thesis. If anything, it strengthens the case for owning the manufacturing and execution layer specifically, because regulatory friction creates exactly the kind of durable moat that sustains long-term pricing power.

Go back to that opening calculation. A $300 billion disease management industry, built on the premise that the underlying cause cannot be touched. The infrastructure companies positioning themselves to touch it are trading at 24 to 28 times earnings.

That is the misprint. And it will not last.

About Scarcity Thinker

Scarcity Thinker looks for what is structurally constrained, mispriced, or overlooked. Metals, equities, crypto, and fixed income when the thesis is there. No asset class religion. No hype.

With many thanks to Mladen Talks Crypto for his clinical perspective and early conversations that shaped this piece 🙏

This article is for informational purposes only and does not constitute financial advice. Do your own research.